08/10/2023

e-invoice Format 电子发票的格式

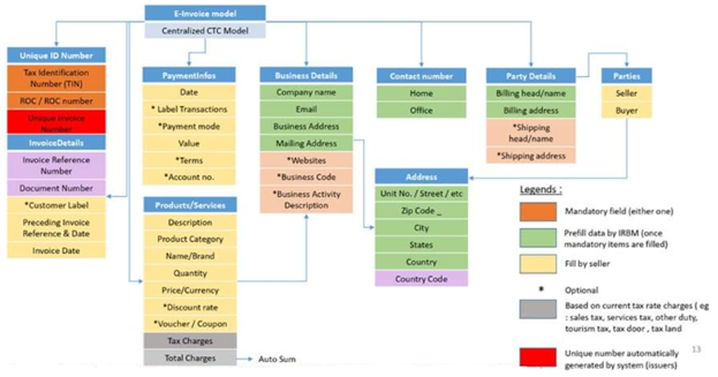

Required Fields :51 required data fields (grouped into 9 categories)

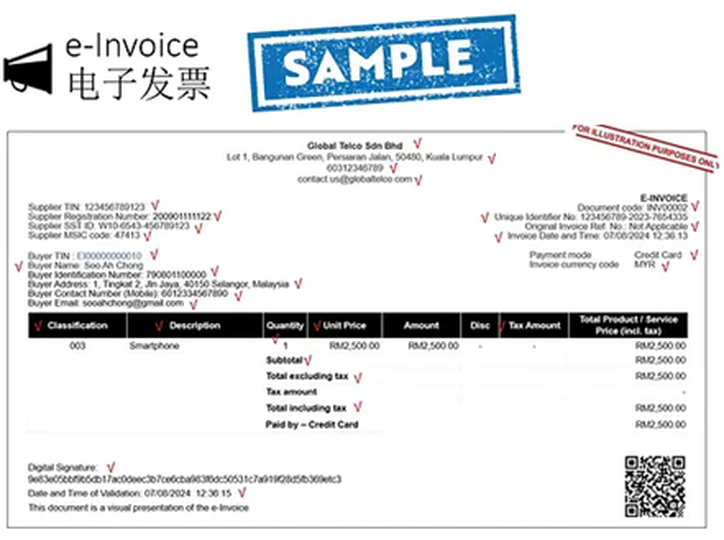

Digital Certificates will be issued to taxpayers to enable them to attach digital signatures to e-Invoices.

Format : For transmission of e-invoice data,only XML or JSON format.

√必填字段:需要填51个必填数据字段(分为9个类别)

√数字证书:开具电子发票需使用税收局提供的数字证书(Digital certificate)进行签名,以验证发

票信息的真实性

√格式:电子发票数据只可以通过XML或JSON格式上传

e-invoice Format 电子发票的格式

1. Address 地址

2. Business Details 业务详情

3. Contact Number 联系电话

4. Invoice Details 发票详情

5. Parties 买卖方

6. Party Details 买卖方详情

7. Payment Info 付款信息

8. Products / Services 产品/服务

9. Unique ID Number 独有识别码(Unique ldentifier Number)

e-invoice Format 电子发票的格式

Additional Mandatory Fields 附加必填字段

Shipping Recipient's Details托运收货人

1)Name 姓名

2)Address 地址

3)Tax ldentification Number 税号

4)Registration number 注册编号

Additional Mandatory Fields 附加必填字段

√ For import and export of goods 货物进出口

05. Who is required to Adopt e-invoicing 谁需要执行电子发票

Transaction Type 交易类型

B2B > B2C > B2G

√e-lnvoice applies to all taxpayers undertaking commercial B2B2CB26activitiesin Malaysia:

√ businesses providing goods and services; and

√ certain non-business transactions between individuals [Guideline will be provided]

√适用对象

√电子发票适用于所有在马来西亚从事商业活动的纳税人

√进行商品和服务销售);及

√个人之间的特定非商业交易(non-business transactions)[指南将在适当的时候提供]

Targeted Group 目标群体

- where goods are shipped to a different recipient and/or address

- 将货物运送到不同收件人和/或地址的情况

Shipping Recipient's Details托运收货人

1)Name 姓名

2)Address 地址

3)Tax ldentification Number 税号

4)Registration number 注册编号

Additional Mandatory Fields 附加必填字段

√ For import and export of goods 货物进出口

- Reference Number of Customs Form No.1, 9, etc. 海关1号、9号表格的参考编号

- Incoterms 国际贸易术语解释通则

- Product Tariff Code [Only applicable to goods] 产品关税编码[仅适用于货物]

- Free Trade Agreement (FTA) Information [For export only, if applicable] 自由贸易协定(FTA)信息[仅适用于出口,如适]

- Authorisation Number for Certified Exporter [e.g., ATIGA number) [For export only if applicable] 核证出口商授权编号(如ATIGA编号)[仅适用于出口如适用]

- Reference Number of Customs Form No.2 海关2号表格参考编号

- Country of Origin 原产国

- Details of other charges 其他收费详情

05. Who is required to Adopt e-invoicing 谁需要执行电子发票

Transaction Type 交易类型

B2B > B2C > B2G

√e-lnvoice applies to all taxpayers undertaking commercial B2B2CB26activitiesin Malaysia:

√ businesses providing goods and services; and

√ certain non-business transactions between individuals [Guideline will be provided]

√适用对象

√电子发票适用于所有在马来西亚从事商业活动的纳税人

√进行商品和服务销售);及

√个人之间的特定非商业交易(non-business transactions)[指南将在适当的时候提供]

Targeted Group 目标群体

- Association 协会

- Body of persons;团体

- Branch:分行

- Business trust商业信托

- Co-operative societies合作社

- Corporations: 公司

- Limited liability partnership;有限责任合伙企业

- Partnership: 合伙企业

- Property trust fund: 财产信托基金

- Property trust; 财产信托

- Realestate investment trust : 房地产投资信托

- Representative office and regional office;代表处和地区办事处

- Trust body : and 信托机构;以及

- Unit trust. 单位信托

Certain B2C transactions where e-Invoices are not required by end consumers

最终消费者不需要电子发票的特定B2C交易

When the end-users do not require e-lnvoices [B2C] 倘若终极消费者不需要电子发票[B2C]

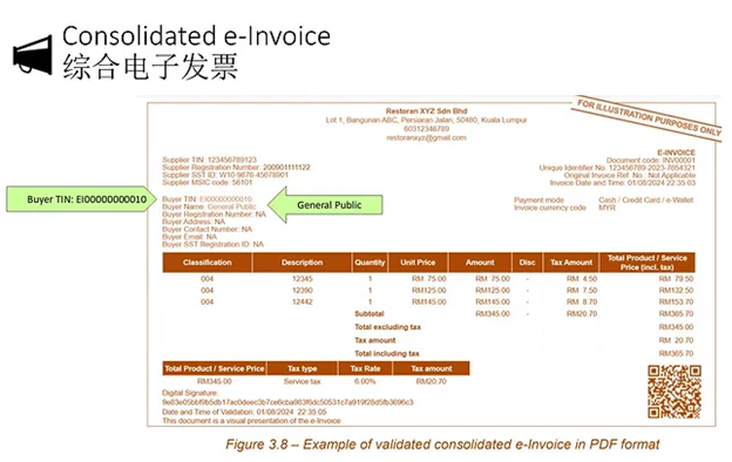

√ Suppliers will be allowed to issue a normal receipt or invoice in accordance with the current practices. 供应商将获准按照供应商采用的现行做法,开具普通收据或发票

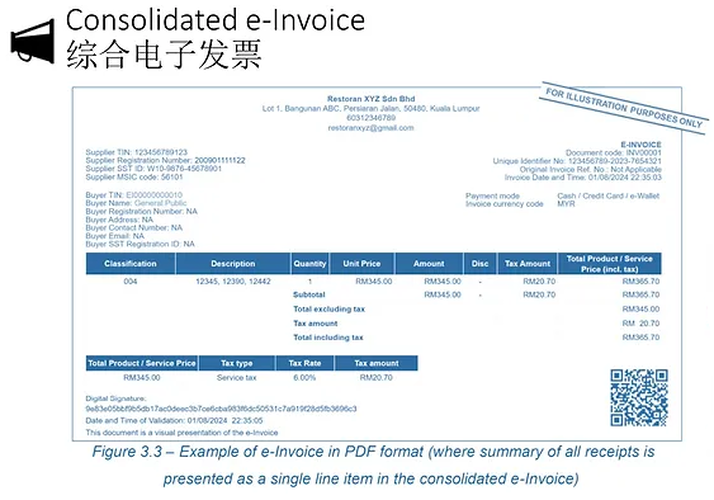

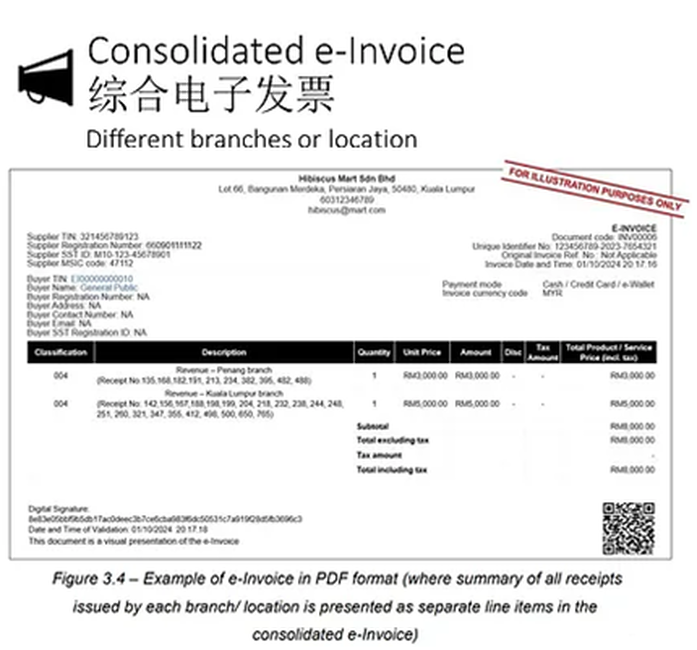

√ Suppliers must aggregate the normal receipts or invoices and issue a consolidated e-invoice

供应商把普通收据或发票合计起来,并开具综合电子发票 (Consolidated e-lnvoice)

√ within 7calendar days after the month end 月末后7个日历日内

When the end-users do not require e-lnvoices [B2C] 尚若终极消费者不需要电子发票[B2C]

If the buyers require an e-invoice after receiving a receipt/bill invoice from the Supplier they must request it within the month of the transaction.

如果买方在收到供应商的收据/账单/发票后需要电子发票,必须在交易的当月内提出申请。

01. Notification to the supplier

02. Request for rejection from Buyer is not allowed

03. The validated e-invoice is not required to be shared with the Buyer

Non-Applicability of Consolidated e-lnvoice 综合电子发票不适用

01. Automotive 汽车

02. Aviation 航空

03. Luxury goods and jewellery 奢侈品和珠宝

04. Construction 建筑业

05. Wholesalers and retailers of construction materials 建筑材料批发商和零售商

06. Licensed betting and gaming特许博彩和游戏商

07. Payment to agents/dealers/distributors 向代理商/经销商/分销商付款

pay-out to winners in relation to betting and gaming

- in casinos and

- from gaming machines are

exempted from e-invoice until further notice

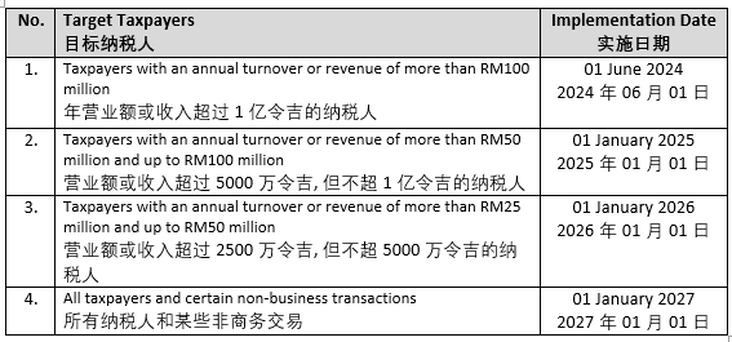

When is the Enforcement Date?什么时候强制执行日期?

Determination of Revenue 年营业额的鉴定

Determination of Revenue 年营业额的鉴定

√ Based on: 根据:

√ annual turnover or revenue stated in the audited financial statements for the Financial year

2022;基于2022财年经审计财务报表中列出的年度营业额或收入。

√ annual revenue reported in the tax return for the year of assessment 2022

根据2022纳税年度报税表中申报的年收入。

Determination of Revenue 年营业额的鉴定

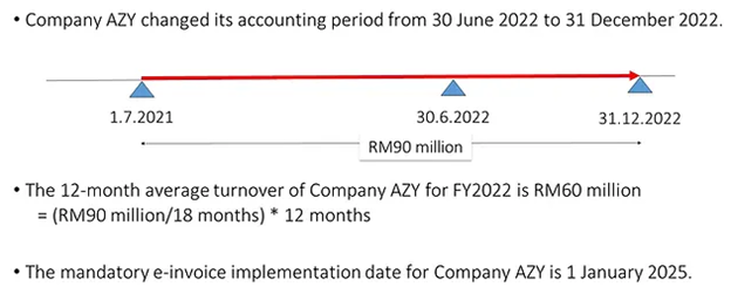

√ In the event of a change of accounting year end for the financial year 2022, the taxpayer's

turnover or revenue will be pro-rated to 12 months for purposes of determining the

e-invoice implementation date.

√ 如果2022财政年度的会计年度末发生变化(比如:更改Year End),纳税人的营业额 或收入将按比 例调整为12个月,以确定电子发票的实施日期。

√ Based on: 根据:

√ annual turnover or revenue stated in the audited financial statements for the Financial year

2022;基于2022财年经审计财务报表中列出的年度营业额或收入。

√ annual revenue reported in the tax return for the year of assessment 2022

根据2022纳税年度报税表中申报的年收入。

Determination of Revenue 年营业额的鉴定

√ In the event of a change of accounting year end for the financial year 2022, the taxpayer's

turnover or revenue will be pro-rated to 12 months for purposes of determining the

e-invoice implementation date.

√ 如果2022财政年度的会计年度末发生变化(比如:更改Year End),纳税人的营业额 或收入将按比 例调整为12个月,以确定电子发票的实施日期。